Some devote half their income to house payments

By

Peter

Healy, Staff Writer Stamford

ADVOCATE

September 9, 2004

Bankruptcy lawyer Elizabeth Austin was looking at condominiums in Stamford in February, intending to shorten her husband's commute to New York City, when she pulled up short of a purchase.

A real estate agent had given the couple hypothetical data that showed how a family with annual income of $120,000 might qualify for a $500,000 mortgage -- meaning, if the loan-to-value ratio was a typical 80 percent, they could afford a $625,000 home.

If you believe the old adage, "Buy as much house as you can afford," the decision is clear. But do the math, and the reality of what you can afford becomes a little bit murkier.

The monthly principal and interest payment on a hypothetical 30-year mortgage for the $625,000 home, carrying a 6 percent annual interest rate, would total $2,997.75, or just about 30 percent of the gross income.

Add in another $1,042 in real estate taxes per month on that Stamford house (at the city's average mill rate of 28.57), and at least $100 for homeowners insurance, and the tab would rise above $4,000 -- more than 40 percent of the hypothetical couple's gross income.

"When I saw the mortgage sheets, my jaw almost hit the floor," said Austin, who works for the Bridgeport office of the Pullman & Comley law firm. "We haven't seen the fallout from this yet. What will happen if the economy takes a dive? What happens if one or both spouses loses their job or gets sick?"

Austin said she and her husband have since given up looking for condos and decided to remain in their home in Trumbull.

[Please read the rest of this article in the archives at the Stamford ADVOCATE website]By

Richard

Lee, Assistant Business

Editor, Stamford ADVOCATE

September 9, 2004

Subsidized housing means the projects.

Or does it?

Public company proxy statements, which reveal the earnings of top corporate executives, show that some of the best-paid people receive a little extra in their paychecks for taking up residence in this area.

Steven Tait, an executive vice president at Stamford-based Gartner Inc. until March 31, 2003, received $101,171 in relocation expenses after taking the job in June 2001. His 2002 salary was $300,000.

Former PanAmSat Corp. Chief Executive R. Douglas Kahn had a contract that paid him $120,500 for commuting and living expenses while the company was headquartered in Greenwich and he maintained his permanent residence in Boston. Kahn made $900,000 in salary and bonus in 1999.

Larry Zimmerman, vice president and chief financial officer of Stamford-based Xerox Corp., received $90,000 in 2002 to help pay for his relocation expenses, plus $800,000 in salary and bonuses, not including stock options.

Whether an executive is buying a home in rural New Canaan or renting an apartment in central Greenwich, housing assistance from the company means less pressure on the executive's wallet but probably some upward pressure on area prices, according to one housing economist.

"People are willing to pay more because they're subsidized to pay more," said Michael Carliner, an economist with the National Association of Home Builders in Washington, D.C.

[Please read the rest of this article in the archives at the Stamford ADVOCATE website]By

Julie

Fishman-Lapin, Staff Writer

Stamford ADVOCATE

September 9, 2004

Nancy Hadden, a real estate agent with William Raveis International, says the high-end market has finally made its way to Stamford.

What convinced Hadden was her recent sale of a 12-room, five-bedroom, five-bath 6,700-square-foot house that was still under construction in the Westover section of the city. It sold for $2.2 million.

The new owners bought based on the blueprints, she said.

But it wasn't until Hadden sat down and pored over the statistics that she realized just how hot the high-end real estate market has become in Stamford.

Ten years ago, six houses costing more than $1 million were sold in Stamford. In 2003, 92 houses sold in that price range, she said.

In the $2 million range, which is the upper-end of the Stamford market, eight houses sold in 2003. So far this year, 10 multimillion-dollar homes have been sold, she said.

The

high-end

market has barely reached

its peak, said Hadden, who works out of the William Raveis

Stamford

office.

She specializes in working with builders, who she says are

paying

hundreds

of thousands of dollars for land, only to tear down the existing

dwellings

to put up a new multimillion-dollar dream houses.

[Please read the rest of this article in the archives at the Stamford ADVOCATE website]

Seven years after the fact, Walter A. Twachtman is still angry.

The lawyer remembers the bitter hearings when he represented a developer who wanted to build 159 apartments for renters earning $35,000 or less near the center of Glastonbury, and the residents who decried the harm "those people" would bring to the town.

A court ruling under the state's affordable housing appeals law ordered Glastonbury to reverse its rejection of a zone change for the complex. But the effort died in 1997, when the town council paid $1.2 million to buy the land where the affordable housing was to be built.

"This is such an act - in my humble opinion - of injustice," the Glastonbury lawyer said recently. "If you listen to the town, they would say, `We did that because we wanted to preserve open space land.' Sounds good, doesn't it? They also made it impossible for us to do our project."

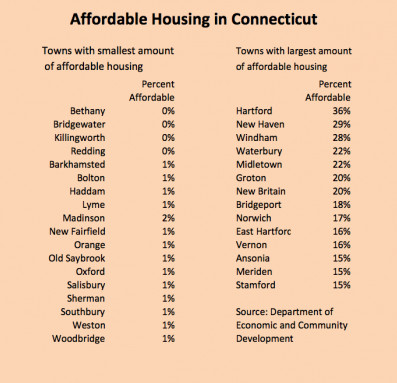

Across the river in Hartford, there's a different story. About four of every 10 homes in Hartford are now government-subsidized for low- and moderate-income people. In Glastonbury, it's about one in 20.

[Please read the rest of this article in the archives at the Hartford COURANT website]Fiscal inequities among Connecticut's cities and towns and an overreliance on local property taxes to pay for municipal services have combined to create "tremendous pressure" on most communities to expand their tax bases by attracting new development. And the most common and damaging approach to development is "fiscal zoning" that allows the raising of local revenue to become the dominant issue, over-shadowing land suitability and regional needs as considerations. These two related conclusions were central to the message that Myron Orfield brought to the economic summit meeting last week in Bridgeport.

From his experience as regional planner, Midwestern state legislator and lawyer, Orfield has made the argument that this pattern of development has had negative results throughout the state. One of these results is that communities are forced to engage in a struggle against each other for the most lucrative development, according to a regional agenda report Orfield has co-authored.

[Please read the rest of this article in the archives at the Westport NEWS website]The Greenwich Housing Authority hopes to build a pair of two-family duplexes on adjacent lots on Hollow Wood Lane in Pemberwick. Each Cape Cod-style duplex would be 2,046 square feet and have two units containing three bedrooms. The units, on the Byram River, will be offered for sale to those meeting affordable-housing income levels. Housing authority officials will present revised plans for affordable-housing units at 14 Hollow Wood Lane to the Architectural Review Committee at a meeting in Town Hall at 7:30 p.m. tonight.

The committee had recommended a handful of aesthetic improvements to the modular houses following the authority's initial presentation on June 2. The houses appeared to be resting on stilts, the committee said, with disproportionately small front windows, and the backs of the houses were "monotonous."

"Some of the conditions they asked for were impossible. That particular site is in the 100-year flood plain, so any house has to have the first floor above flood levels," said housing authority board member George Yankowich, a local builder and developer. "The houses look like they're up on stilts and they wanted to eliminate that, but technically it's not possible."

[Please read the rest of this article in the archives at the Greenwich TIME website]Commonly called a housing "mandate," the statutory provision actually does not require municipalities to build or cause to have built a single unit of affordable housing. But it does provide developers the opportunity for fast track court appeal when they are denied permits by municipal land-use approval bodies for projects that include an affordable component as a set-aside from the balance of the units in the project that are priced for the market.

The statute also places the burden of proof in such appeals on the municipality to prove that the denial was based on a legitimate exercise of its state-delegated power to adopt regulations that protect health, safety, and general welfare, under the so-called "police powers" that are reserved to the states under the U.S. Constitution. Those cities and towns that meet the state's definition of affordability at the 10 percent level are exempt from the fast track appeal, and those that are making progress toward that goal might obtain a three-year moratorium from the measure.

And

therein

lies the problem. The

state standard for defining affordability is local area or state

median

income level, whichever is lower. The recently released

report of

the committee for Westport Workforce/Senior Housing (WFSH)

estimated

that

the qualifying income level for a family of two would top off at

$66,000

under the state statute.

[Please read the rest of this article in the archives at the Westport NEWS website]

A study commissioned by the city two years ago found that Stamford has about 4,600 affordable housing units, putting it ahead of neighboring municipalities. But the report also found that Stamford needed as many as 8,000 more affordable units. The new guidelines can't fill that need, Principal Planner Norman Cole said. The rules seek to include a few affordable units in each market-rate development. So results would have to wait for private firms to build new projects in a city that is increasingly built up.

"We would be very lucky if we could do 100 affordable units a year," Cole said. But the new rules have advantages over developments by agencies that build exclusively affordable units. "The nice thing for us is that it is free of public subsidy," Cole said. In exchange, private developers would get to add a few more units than they would under existing zoning. This "bonus density" would help offset the cost of building the moderate-income units, city officials said.

The city decided it had to do something to encourage affordable housing, in part because the state and federal governments have pulled back from supporting such developments in recent years. Although a state budget has not been finalized, early drafts called for the reduction of Connecticut Housing Finance Authority funds. Meanwhile, the U.S. Department of Housing and Urban Development has prepared to cut Hope VI funding in future years. Both programs have significantly contributed to Stamford's affordable housing in the past.

[Please read the rest of this article in the archives at the Stamford ADVOCATE website]"Certainly, Stamford is a leader not only in the state but in the country as far as I'm aware in promoting affordable housing," said Richard Redniss, president of engineering and planning firm Redniss and Mead, and a member of the state's Blue Ribbon Commission to Study Affordable Housing. The number of housing projects completed or in the process of approval in Stamford in the past 10 years is significant, officials said, ranging from the renovation of 330 units at Southfield Village, which will be 70 percent affordable, to the Park Square West complex, which will contain 20 percent affordable units, aimed at families with incomes of 50 percent of the area's median income to the Avalon at Greyrock Place complex, which contains 38 units below market rate.

Spurring that growth is the city's effective use of zoning regulations that require affordable units to be included in development projects and incentives for developers. "I think what we've done well is take a formalized approach by having both requirements and incentives," said Mayor Dannel Malloy. Inclusionary zoning is not a new idea, having been around for close to 15 years in Stamford and Norwalk, but only recently are communities fully recognizing its potential.

"It is one of the most powerful tools available for communities to create affordable housing," said Alan Mallach, a housing and land use consultant who teaches urban planning at Rutgers University to a panel convened by Norwalk Mayor Alex Knopp last fall. Although inclusionary zoning has been around for some time, Stamford has only recently tied in incentives for developers, an evolution that came from some early missteps during Malloy's tenure. "We let some things get out the barn door before we closed it," Malloy said. Developers now receive density bonuses and tax abatements for adhering to affordable housing requirements. It came as a surprise to Malloy early on that so many people in the area were looking for places to live. "I don't think we anticipated the pent-up demand for housing," Malloy said.

[Please read the rest of this article in the archives at THE HOUR (Norwalk, CT) website]"I'm concerned every day that these people may find employment closer to home and may take those opportunities," said Ivory Tucker, chief executive at Norden Systems, who said that he has an "aging work force" and needs to hire more younger employees. But, Tucker said, finding young engineers and manufacturers who are willing to come to the area has proven difficult. "One of the things that happens, especially with new graduates, is that getting them to come to the area (is harder) because of the high cost of living and the lack of available housing," Tucker said.

[Please read the rest of this article in the archives at THE HOUR (Norwalk, CT) website]"We thought that housing for working families was something the council could tackle more easily than the housing crisis overall," said Council President Matthew Miklave, D-District A. "When I was growing up, our parents' goal was to build a community and maintain a community where their children could live if they so chose. In order to do that, you have to have lots of housing choices for people so they can elect to stay in the community where they grew up." As Chamber of Commerce President Edward Musante explains it: "Our members are very upset there's not enough housing for their workers." Joseph McGee, vice president of public policy and programs for the Business Council of Southwestern Connecticut (SACIA), agrees.

"If

you

don't provide a vibrant range

of housing options for people, you'll lose your labor force and

economic

competitiveness," he said. "We're not talking about public

housing,"

said Common Councilwoman Barbara Hudgins, D-at large. "People

are so

confused

about the word 'affordable' that Matt wanted to find a different

name.

It's not what in the past have been called 'projects.' And it is

not

special

needs housing for disabled people or mentally ill people or

halfway

houses."

As much as the council is trying to define what its initiative

is not,

in order to pare down its goals to a more manageable level,

"housing

for

working families" is also politically a much more acceptable

choice of

words for a group of 15 Democrats facing re-election in

November.

Miklave

acknowledges that the label "housing for working families" was a

conscious

public relations move because the term "affordable housing" not

only

creates

confusion but has also been "demonized over the years." "As soon

as

they

hear

about it, some people stop listening,"

Miklave said. "If you talk about an affordable housing project,

people

would say 'no, no, no.' But if you say you want to make it

easier for

cops,

firefighters and teachers to live in the community they serve, a

lot of

people would say 'yeah.'"

MILFORD

—

The fate of AvalonBay’s

proposed 284-unit complex at Wolf Harbor and Wheelers Farms

roads is

back

in the hands of the city, following a Supreme Court ruling

Wednesday

that

denied the developer’s request for sewer service.

The court denied the Wilton-based

affordable housing giant...

And an earlier

article, from another CT area...

Saturday, January 19, 2002 - 6:46:54

AM MST

Officials expect housing

to come

By FRANK JULIANO - fjuliano@ctpost.com

MILFORD -- City officials for the first time have conceded that a Wilton developer will get to build a controversial apartment complex on Wheeler's Farms Road, despite their vigorous opposition.

"Someday, somehow, that thing is going in," state Sen. Winthrop Smith told about 50 elderly residents at the Milford Senior Center Friday. "It may take five years, but that state law was written for them, and when they go to court, they are going to win," Smith conceded.

Mayor James L. Richetelli Jr., who also attended the center's annual legislative breakfast, agreed that the state's Affordable Housing Act, which supersedes local zoning regulations, presents an almost insurmountable obstacle to municipalities trying to keep dense development out. AvalonBay Communities Inc. is proposing to build 284 apartments on 43 acres at the corner of Wolf Harbor and Wheeler's Farms Road, setting aside 25 percent of the units for families earning less than Milford's median income, pegged by federal officials at $60,000 for a family of four.

The

Inland

Wetlands Agency approved

the project Wednesday with conditions that reduce the number of

apartments

to 228. The Planning and Zoning Board will conclude

its public hearing on the proposal

Tuesday night, 7 p.m. in City Hall. "It is my position

that we'll

do everything we can to keep AvalonBay from coming in,"

Richetelli

said.

"But they are a national company with tons of money and they

keep

coming

after you."